Profession & Future

By Ian Schick, PhD, Esq

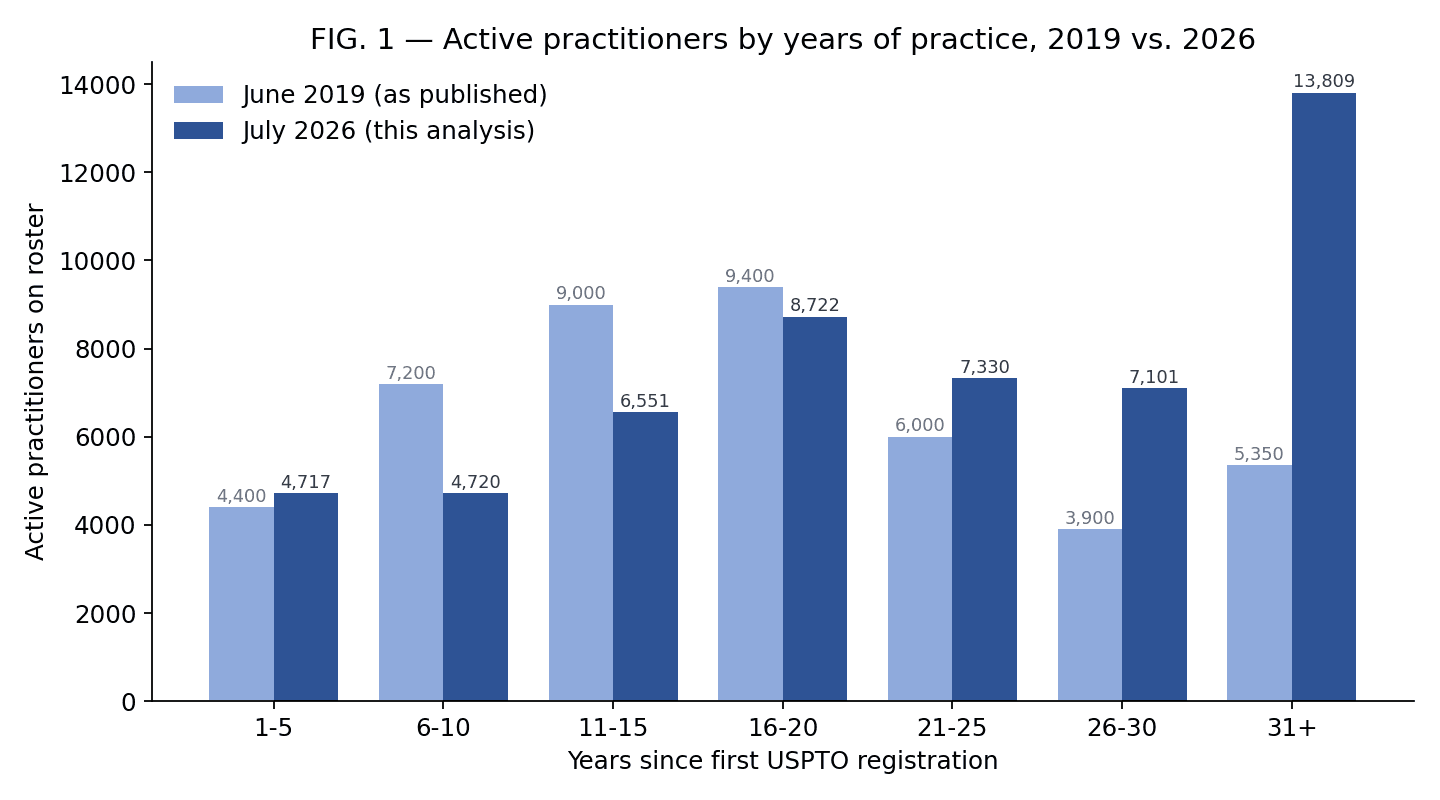

In July 2019, I posted a histogram to a company blog and it became one of the ten most-read guest articles on IP Law360 that year. The chart showed active patent practitioners binned by their earliest year of USPTO registration, and it said something nobody wanted to hear: "There are more active practitioners today with 21-25 years of practice experience than there are active practitioners with 1-5 years experience."

I predicted the imbalance would deepen, that retirements would thin the big mid-career cohorts with no one behind them, and that the industry could not "continue to defy the basic principles of economics forever." Seven years is long enough to check. Last week I downloaded the current OED practitioner roster, 53,453 names, and re-ran the analysis.

What I got right, and more right than I wanted

The marquee claim from 2019 is still true, and it is worse. There are roughly 7,300 active practitioners with 21-25 years of experience today, against 4,717 with 1-5 years. The ratio was 1.36-to-1 in 2019. It is now about 1.55-to-1.

The whole distribution has slid to the right (see FIG. 1). In 2019, half of all active practitioners had 16 or more years of practice, and I called that shocking. Today, half have 21 or more years, and two-thirds have 16-plus. The average practitioner gained roughly five years of seniority in seven calendar years. A workforce that was replacing itself would have gained zero.

And the pipeline never recovered. New registrations ran around 1,800 a year in the late 2000s. By 2019 they were down to about 1,000. I noted then that the youngest cohort would grow by "roughly 500 practitioners" in the back half of the year. The trough came in FY2020-22, in the low 800s a year, before a modest recovery to 1,048 in FY2025 (see FIG. 2). Intake is still more than 40% below the FY2005-10 average, and exam sittings in FY2025 were fewer than in FY2015. The 6-10 year cohort, the people who should be carrying today’s drafting load, numbers 4,720. In 2019, the equivalent cohort was 7,200.

What I got wrong

I predicted "major falloffs after 20, 25, and 30 years of practice" would hollow out the big 2000s cohorts, and that the bandwidth shortage would become "increasingly acute." The falloffs did not show up.

The 2005-2009 registration vintage, about 9,000 strong on the 2019 roster, still has roughly 8,600 names on the roster today. The 2010-2014 vintage is essentially untouched. Meanwhile, the 31-plus-years population has swollen. Two explanations fit the data, and I cannot separate them: the bar’s seniors are not retiring on the schedule their predecessors kept, or the roster has stopped noticing when they do. OED has not run a purge survey in over a decade. Either the cliff was postponed by people who kept working, or it is hidden behind stale records. Both readings should worry a managing partner more than my 2019 chart did.

Here is the two-part distinction I under-weighted in 2019: a roster counts names, while a workforce is measured in hours. Those are different things. A 68-year-old of counsel who reviews four applications a year and a 34-year-old associate drafting sixty both count as one name. The roster grew from about 45,000 to 53,000 while the drafting-age middle of it thinned.

I was also wrong about demand. In 2019 I leaned on "an ever-increasing trend" in annual filings. Filings plateaued instead. The USPTO received just over 600,000 utility applications in FY2025, roughly where the mid-2010s left off. Flat demand bought the supply side time I did not think it had. And the acute, visible crisis (spiking fees, missed filings, firms turning work away) never made the trade press. The fear was reasonable. The mechanism was wrong.

The surprise nobody predicted

The newest entrants are not who they used to be. Of practitioners registered in the last five years, 62% are patent agents rather than attorneys: 2,922 agents against 1,795 attorneys. Walk back through the cohorts and the gradient is unmistakable: 29% agents among the 2006-2010 entrants, 33% for 2011-2015, 43% for 2016-2020, then the jump (see FIG. 3). Some of the recent agents will sit for a state bar and convert, so the older figures understate agent intake somewhat. The trend survives any reasonable correction.

Think about what that selects for. An agent’s practice is preparation and prosecution: no litigation escape hatch, no M&A rotation. The people still choosing this profession are choosing the drafting work itself, at a lower cost structure, typically closer to the technology. The patent bar is aging, and it is quietly specializing toward production.

Where the capacity went

So the 2019 arithmetic held (fewer entrants, older bar, flat fees), and yet the system did not buckle. Something absorbed the load.

In 2019 I argued that if you think about practitioner efficiency "in terms of hours per application instead of dollars per application, then leveraging new technologies starts to make a lot of sense, specifically automation." That was the one paragraph of the piece that named the resolution, and it turned out to be the load-bearing one. I was early. I wrote "the inflection point seems to be roughly now," and the honest reading is that the inflection arrived around 2023-2025, when drafting systems stopped assisting with typing and started owning the content generation. But the direction was never in doubt, because nothing else on the supply side moved.

When a workforce shrinks at the bottom and demand holds, the capacity doesn’t disappear. It relocates into fewer, more leveraged practitioners who direct more work per unit of judgment. That is what the data shows already happening: a smaller drafting-age core, a rising share of production-focused agents, and per-practitioner throughput that must be climbing simply for the arithmetic to close. The typing is leaving the profession. The judgment is concentrating.

That is why I think the agentic production model wins this decade. The demographics left no alternative. My 2019 critics argued the bar would replenish itself. Seven years of roster data say it declined the invitation.

Grade the 2019 piece however you like. I’d give the diagnosis an A, the timing a C, and the proposed resolution the benefit of having been the only mechanism that showed up for work. The next audit is due in 2033. I expect the roster to be smaller, the median practitioner to be directing rather than drafting, and the firms that planned for that practitioner to own the decade.

The cliff was never going to look like a crash. It looks like this: the same work, done by fewer hands, at higher leverage. Demographics set the deadline. Automation met it.